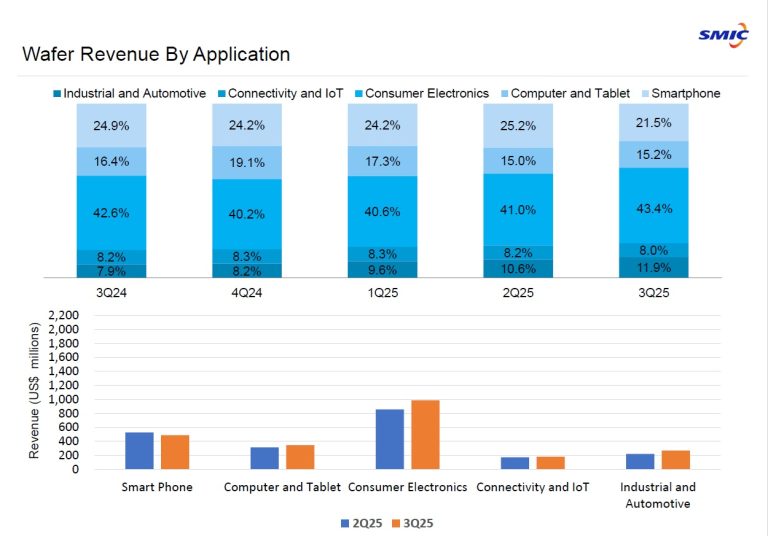

China’s largest foundry, SMIC, revealed a surprising twist in its latest earnings update: while its third-quarter revenue rose, the smartphone segment fell to 21.5 % of its business from 25.2 % in the prior quarter. The company attributed this drop partly to memory-chip shortages that are forcing smartphone manufacturers to hold off on placing new orders for early 2026. According to the report by TrendForce Corp., this cautious behaviour is an unusual turn for a device category typically driven by forward-planning and high volume.

Why the memory crunch is even affecting other chips

The underlying issue is that DRAM and NAND supply is tightening sharply. Memory makers are redirecting capacity toward high-bandwidth memory for AI servers and data centres, leaving fewer chips available for smartphones. Even if smartphones are ready with processors, sensors and display components, without the memory the assembly chain stalls. SMIC’s co-CEO noted that this dynamic is the exact reason many OEMs are refraining from committing to non-memory chip orders, creating a “crowd-out” effect across the semiconductor supply chain.

What this means for smartphone brands and foundries

For smartphone makers the implications are immediate. With memory becoming a bottleneck, some are delaying launch plans or trimming expected production volumes. Pricing pressure is likely too: brands may need to negotiate lower prices for logic ICs (like those made by SMIC) or absorb higher BOM (bill of materials) costs to maintain retail pricing. For foundries like SMIC, this means that while demand for logic chips remains strong, the flow of orders becomes more erratic and tied to memory-availability risk rather than just logic capacity.

Broader impact on smartphone pricing and product strategies

The shortage is likely to change how phones are built and priced throughout 2026. If memory costs continue rising, manufacturers may:

– Launch models with lower RAM or storage configurations to keep costs in check

– Delay premium launches until memory supply stabilises

– Shift marketing focus toward features less dependent on large memory footprints

These changes may also push some OEMs to prioritise regions or segments where they have stronger memory commitments, leaving other markets with fewer new devices or slower rollout schedules.

Why the timing matters now

The crunch is coinciding with industry-wide shifts: the AI-server boom is reallocating memory resources, legacy DRAM lines are being phased out, and major OEMs are trying to lock down contracts during a period of extreme volatility. Because memory fabs take one to two years to scale capacity meaningfully, the disruption is likely to persist well into 2026. That means smartphone supply chains that typically plan months ahead are now navigating uncertainty.

Implications

For device buyers this means you may see higher prices, reduced memory specs, or slower launches throughout 2026. For OEMs and components suppliers it means the memory segment is no longer a peripheral risk, it’s central to device availability and pricing. And for foundries like SMIC, the message is clear: “logic-chip demand alone” isn’t enough anymore, your fortunes are increasingly tied to the memory realm and how that bottleneck unfolds.

Source: Trend Force